Disclosure: I opened a position in DIDI on 7/27. Since writing this piece on 7/13, DIDI, along with many Chinese stocks have experienced extreme volatility. During that period of extreme fear, I thought DIDI’s risk/reward ratio became favorable.

Introduction:

DiDi stock IPO’d in the US recently. It was the biggest US listing by a Chinese company since Alibaba. Normally, this would be a great cause for celebration for investors, but the party was short lived. 2 days later, the Chinese regulators announced a probe into DiDi’s data security policies and asked the company to halt all new user registration in China (link). Since then, all the DiDi apps were taken down from the Chinese app store, though existing apps will still function normally. The stock price had also taken a beating since, down 20% from its IPO price and shedded $10B in market values in the past 2 weeks.

But is it really that bad? DiDi has become a structurally important company to the Chinese economy and has a near monopoly on the Chinese ride hailing market. Most people in China that use the app likely already have it. Could this actually be a buying opportunity?

DiDi Overview & Brief History

DiDi first started in 2012. The origin story is similar to other startups. The founder Cheng Wei found it difficult to get a taxi during his frequent travels, particularly during bad weather. One time in Beijing, he had to wait in the rain for a good 30 minutes before finally hailing down a taxi. He thought, there must be a better way than this. And so, DiDi was born.

Over the next 9 years, he managed to built a massive ride hailing business. To illustrate the sheer scale of DiDi, here are some key highlights about the company’s operations:

- At the end of Q1 2021, they had 493 million active riders and 15 million active drivers on their platform.

- Within China, they have 90%+ market share in ride hailing. In Q1 2021, DiDi facilitated 2.2 Billion (yes a B) trips. This is 50% more than Uber (valued at 2x DiDi’s current market cap) across the entire world!

- Outside of China, they are also investing and expanding aggressively. Their first international market was Brazil in 2018, and since then have expanded to 16 other countries and now facilitates more than 400M transactions/quarter.

Getting here wasn’t easy. Along the way, they had to beat out 30 other domestic competitors as well as Uber, who up until that point had steamrolled their competition in every market. At the height of their competition, both companies were losing ~$200M every month to eke out market share. In the end, it was Travis Kalanick who blinked first and sold Uber China to DiDi for a 17.7% stake.

Uber was the “final boss” in DiDi’s bid to dominate China’s ride hailing market. After successfully kicking Uber out, DiDi now has a near monopoly in the domestic ride hailing market and is aggressively expanding to other verticals. The final vision for DiDi isn’t a taxi ride hailing company, but an integrated mobility company that spans across all modes of transport.

I had always admired the company’s ambition and execution capabilities from afar. With its recent IPO, I wanted to take a closer look at the business under the hood and see if it’s something worth adding to the portfolio, despite the regulatory headwind. I structured this deep dive into 4 key questions, each presented with a bull case and a bear case argument. At the end I’ll also give my closing summary and value judgement on the company.

The 4 questions to explore are:

- How big can DiDi’s ride hailing business in China become?

- What’s DiDi’s probability of success in international markets? Can they replicate their success domestically elsewhere?

- What other adjacent verticals can DiDi enter in the future and how attractive are those businesses?

- What are key regulatory risks for DiDi and how to price that into the stock?

Let’s take a look at these questions one at a time

How big can DiDi’s ride hailing business become in China?

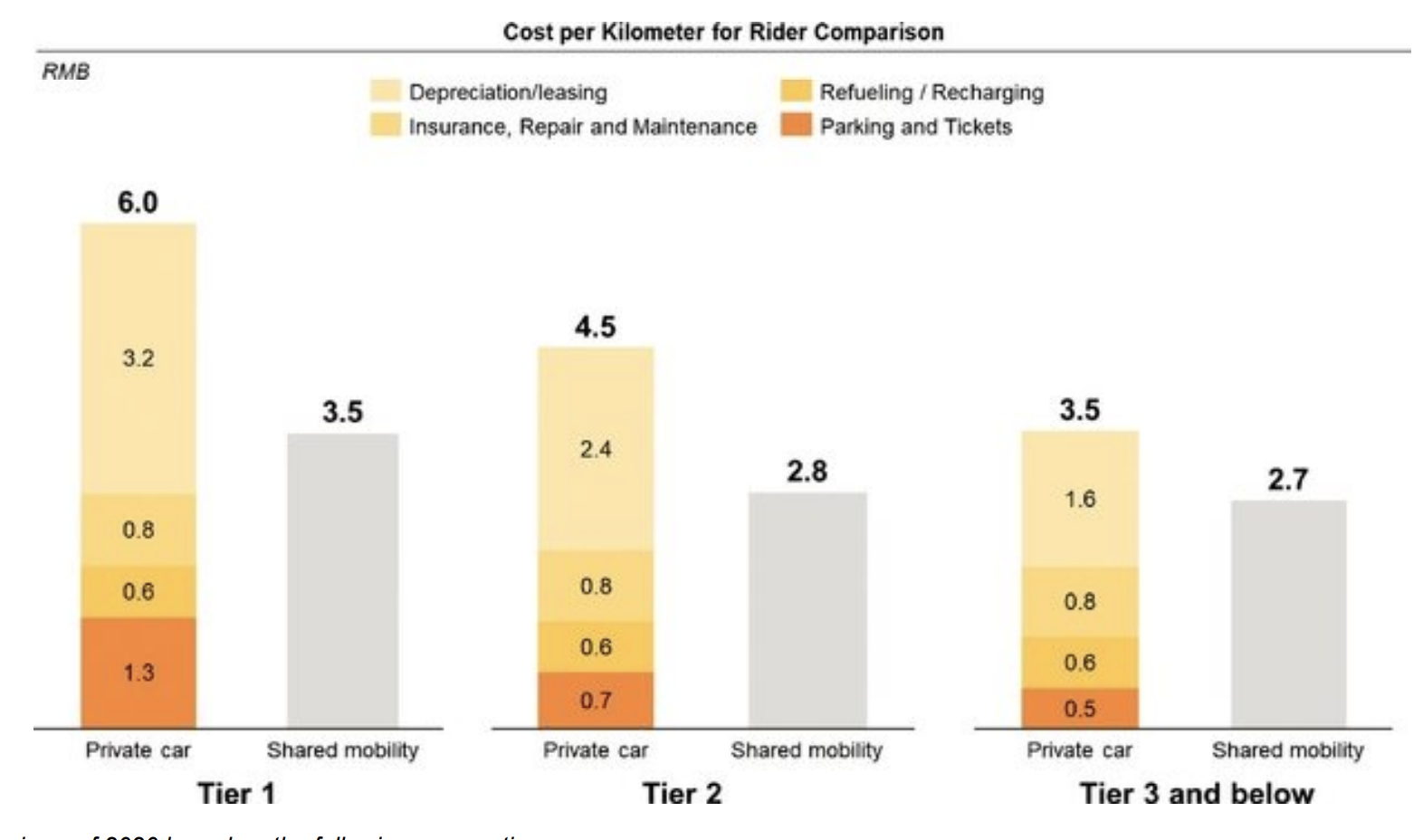

Shared mobility is the future of transport. DiDi is China’s domestic champion and quickly becoming a global leader. In investing, there’s a saying that you shouldn’t bet against the future.

Currently, the private car usage rate is <5%, meaning the other 95% of the time, it’s just sitting there losing money. The shared mobility model can lift that utilization rate up to 70% in dense urban environments. It’s a far more productive use of the asset compared to traditional private ownership.

In fact, this shows up in the data. In China, ride hailing is actually cheaper than private ownership.

There are a few reasons for this:

- China has a massive urban population and that rate is increasing. It was reported that in 2019, 60%+ of the 1.4 billion Chinese people live in an urban area. (link) Over the last decade, the urbanization rate has increased by a full 10 percentage points. As a result of this, China has a massive traffic congestion and pollution problem.

- To combat this, China has placed strict limits on vehicle ownership, causing private ownership cost to go up. For example:

- In first-tier cities, there’s a lottery system to first become eligible to purchase a vehicle. The chance of winning is <1%, which means many people wait years before they obtain the right to buy a vehicle.

- It cost 75k – 100k RMB (10k – 12k USD) for a license plate even if buyer wins the lottery

- In some cities, residents are only allowed to use their vehicles on certain days of the week.

These restrictions, along with overall lower purchasing power means that only 1 out of every 2 households owns a car. In the US, it’s the reverse. Every household owns on average 2 cars! Can you imagine if tomorrow, 75% of vehicles on the road vanished, how much more popular Uber/Lyft would be? It would overnight be a trillion dollar company!

With time, ride sharing will replace private car ownership altogether. Today, there are 280 million passenger vehicles on the road in China and growing. That’s equivalent to 5 trillion kilometers driven every year and 35x the mileage driven by taxis. Let’s be conservative and only assume we will convert 20% of that 5 trillion miles into ride hailing, that’s an incremental $450B USD market of untapped market in China alone and a multi-trillion market globally. As the cost of rides come down and people get used to the idea of shared mobility, the addressable will continue to expand.

The catalyst for this change will be autonomous-driving technology. Currently, the driver accounts for ~50% of the ride hailing cost / trip. By eliminating the driver, ride hailing not only becomes safer, but also significantly more affordable. The cost advantage will be too great for most consumers to opt for private car ownership.

In the self-driving arena, the pace for DiDi’s autonomous driving unit is clearly speeding up.

- DiDi raised $800 million for its self-driving unit in 2021 (link 1, link 2)

- DiDi recently showcased some of their progress back in April 2021 (video below) where they were able to drive around the city of Shanghai for 5 hours without a single disengagement.

- They have signed strategic partnership with Volvo and Nvidia to develop the next self-driving platform (link)

DiDi knows that autonomous driving is intricately linked to the future of its ride hailing business and is investing heavily in this area. When self-driving becomes a reality, DiDi will be one of the leaders in it and stands to reap the benefits.

In summary, it’s still Day 1 in DiDi’s ride hailing business and there’s massive room for growth ahead.

DiDi’s ride hailing business has maxed out. The argument that private vehicle ownership will shift to shared ownership is fundamentally flawed, for the simple reason people don’t buy cars because it’s the most economical choice. Despite the fact that ride hailing is already cheaper than private ownership in China, the number of vehicles being sold to individuals every year continues to go up! If shared mobility is the inevitable future, shouldn’t that number be coming down instead?

Owning a car is a symbol of freedom & status. Particularly in China, it’s a signal that you have a solid financial base. There are also many intangible benefits associated with car ownership that you otherwise wouldn’t get with ride hailing. For example:

- You can take spontaneous trips faraway on the weekend.

- You can put things in your car while you are out and about instead of carrying them everywhere.

- In heavy rain and snowstorms, you don’t have to worry about whether you’ll be able to get a ride home.

These are all “luxuries” that come with private ownership that ride hailing simply can’t provide. Most people are willing to pay for these benefits.

Furthermore, I believe the regulation limiting vehicle ownership is transitory. Those rules were made early on to ease pollution concerns. As China’s EV adoption increases (currently 10% nationwide and 20% in tier-1 cities), the air pollution concerns become moot. In fact, to promote EVs on the road. The Chinese government has specifically lifted license plate quota restrictions in an effort to promote EV (link). As EV penetration goes up in the country, I expect the quota restrictions to lift. .

So now when we look back to the present, we see that the ride hailing market in China is already quite saturated. Of the 490 million urban dwellers between age of 15 to 64 (core DiDi addressable segment), 377 million are already active riders on its platform. This suggests little user growth upside ahead.

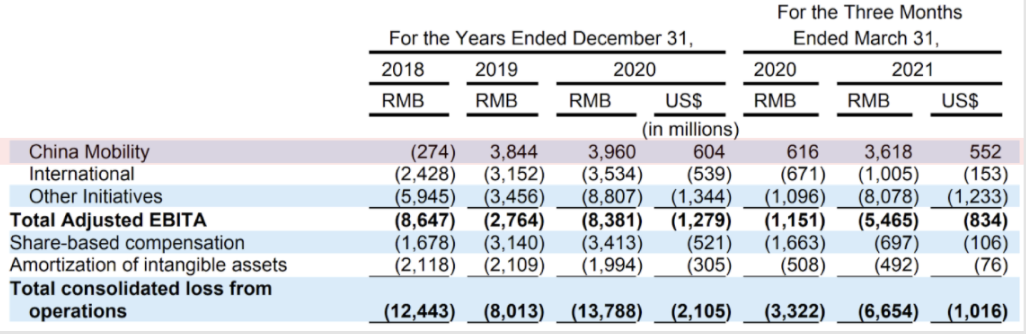

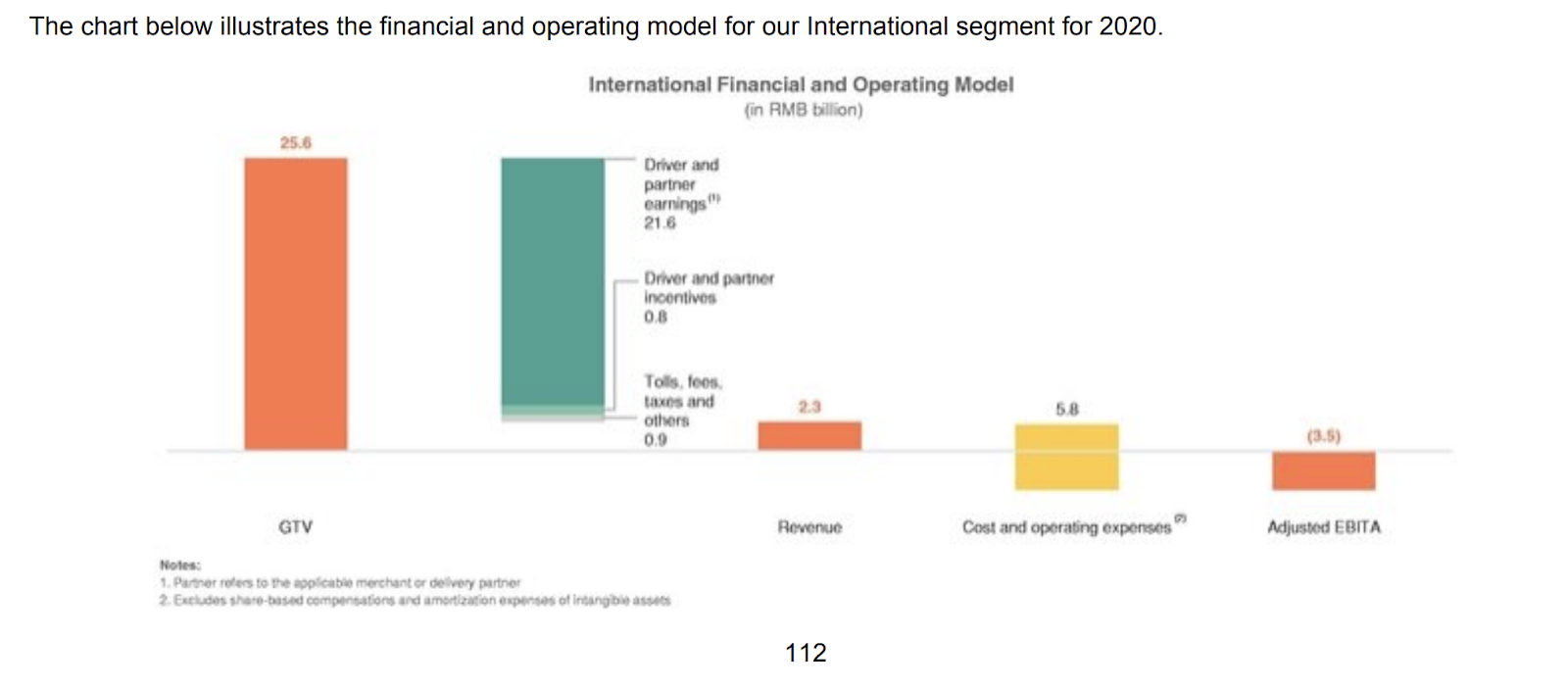

On the frequency side, the growth is also limited. I estimate that ride hailing already accounts for ~36% of all taxi market share and has stabilized. This is evident in DiDi’s IPO prospectus as well. Since 2018, DiDi’s China mobility business has stalled. Both transaction volume and GTV shranked each year between 2018 and 2020. In fact, the only way for DiDi to maintain growth over the past 2 years was to double its take rate from 9% to 17%. In Q1 2021, that ratio reached 26%. For comparison, Uber’s take rate is ~22%.

While some increases are expected and even reasonable, excessive increases like the above are not healthy for the broader ecosystem. Every incremental dollar DiDi extracts this way either takes away from their driver’s direct earning or increases consumer cost. I believe it’ll be very difficult for DiDi to increase their take rates any further without drastically reducing the size of its business (link).

The other giant elephant in the room that nobody likes to talk about is that DiDi’s domestic ride hailing business is not very profitable, despite the fact that it is a monopoly. They had an adjusted EBITDA of $600 million USD prior to SBC and amortization in Q1 2021. Let’s pretend those pesky non-cash expenses don’t exist and we give it a 15x P/E multiple on the annualized adjusted EBITDA (generous for a low business that’s reached maturity), that’s would imply DiDi’s domestic ride hailing business is worth ~$33B today.

Lastly, when thinking about the future of ride hailing, you have to think about autonomous driving. While this will certainly benefit the consumer and a big boost for the ride hailing market as a whole. I believe DiDi’s specific position within this industry will be worse off because of it.

There are a few reasons for this:

- One of the great barriers to entry for ride hailing is the ability to stand up a 2 sided marketplace of riders and drivers. When self driving becomes a reality, the driver side becomes a simple vendor relationship. Whoever has the biggest bank account and can acquire the largest fleet of self-driving cars will be the biggest winner. Many new competitors will come into this market, further commoditizing the business.

- DiDi is highly reliant on other partners to build its self-driving technology. DiDi is a business that excels in its operational execution, it’s innovation often comes from applying new business models to existing industries and leveraging well understood technologies to gain efficiencies within. However, it is not a company that has deep technology expertise. In this type of dynamic, it’s highly likely that the technology provider is the one with pricing power, and DiDi will be unable to extract incremental profit from this technology. More than likely, these technology providers will also be competitors that offer their own version of autonomous ride hailing service.

You can think of the future outcome for DiDi in the following quadrants

When looking at the chart above, it’s clear that the only good outcome is if DiDi becomes a leader in self-driving tech ahead of everyone else (Waymo, Tesla, Cruise, Baidu, Aurora, Pony.AI etc.). Based on what’s currently known to the public, I view that scenario as extremely unlikely. They also don’t have an equity stake in any of the other self-driving startups, so its ability to acquire the technology ahead of everyone else is low.

The realistic outcome that DiDi can hope for is either:

- Self-driving doesn’t become reality and it can maintain current status quo

- Self-driving becomes reality, and DiDi is able to purchase the technology without drastic reduction in its unit economics.

In summary, DiDi’s existing ride hailing business is a stagnant one with little prospect for growth. In addition, self-driving is an existential risk for DiDi and the likelihood of a good outcome is low should the technology become a reality.

What’s DiDi’s probability of success in international markets? Can they replicate their success domestically elsewhere?

DiDi’s international expansion is very encouraging. Less than 4 years in, they are already in 17 countries and the rate of expansion is accelerating.

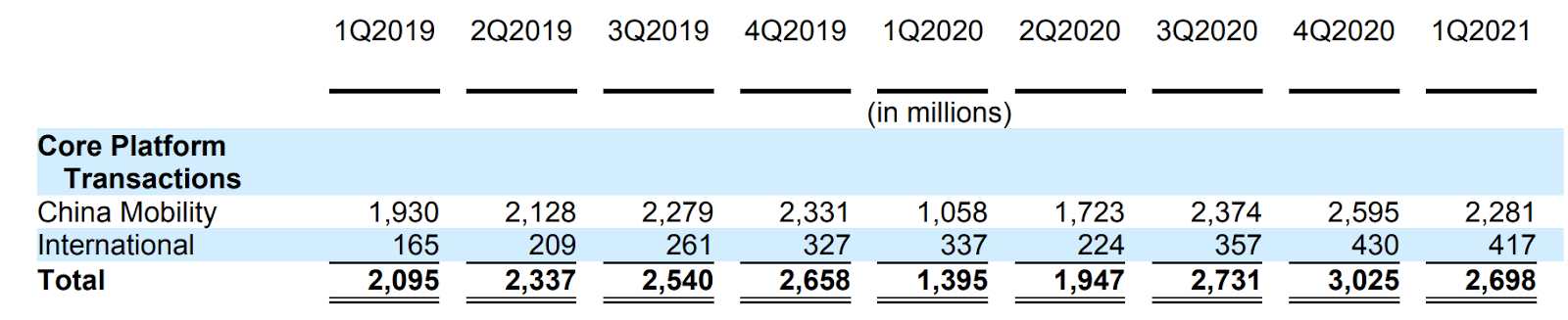

Transactions volume is up 150% between Q1 2019 and Q1 2021.

Up until this point, Latin America has been the key battleground. This is because Latin America is not only a big market, but also one with a lot of similarities to China.

- Latin America as a region has a population of 650 million, of which 65% are between the ages of 15 and 65 and 80% reside in urban areas (even higher concentration than China!). Assuming similar ride hailing penetration rate against Taxis, it would suggest Latin America as a whole is worth ~$70B USD in GMV, roughly the same as the Chinese market.

- The growing population poses new challenges to transportation and other related infrastructure. The cities like Sao Paulo, Mexico, Bogota cannot afford to put any more vehicles on the road without an infrastructure overhaul (similar problem to China).

- Large metros are already crowded with vehicles making it jammed in peak hours (see São Paulo, a city with a 180km traffic jam). As a result, commuters are hesitant to own personal vehicles. Latin America is still reliant on conventional public transportation such as buses, trains, and subways (see the pattern here?).

We shouldn’t trivialize these challenges, but they are precisely the issues that DiDi had to overcome in China. Their experience domestically will be very useful and help them move quickly. If DiDi can become the go-to transportation layer in these countries, these efforts will pay big dividends down the line.

Unlike Didi’s domestic business, there’s significant room for growth within Latin America. User penetration in the region is generally less than 30%, many less than 20%. A DiDi spokesperson said in an interview back in 2019: “less than 3 in 10 Mexicans use ride-hailing, and barely 1 in 10 use food delivery.“ If DiDi executes well, there’s a lot of open space to grow into (ink).

More encouragingly, DiDi is growing in this market while also taking shares away from Uber. Prior to DiDi’s entry, Uber was practically a monopoly in the region. Based on both company’s SEC filings, we can see DiDi has been consistently taking shares away from Uber over the past 2 years. It is now estimated to be close to 25%, which is consistent with field reporting (link).

DiDi was able to achieve these results because it is more readily willing to adapt their model to local market needs compared to Uber. Also, as a new entrant, DiDi took advantage of the bad history that Uber had with the taxi drivers and offered them a better alternative. If Uber was arming the rebels with AK47s, then DiDi is providing the incumbents with their own M16s.

Cheng Wei and Jean Liu are ambitious founders with a clear vision. So far, they are running laps around Dara & team in Latin America (link).

This is strong evidence that DiDi didn’t just win China because it had the backing from the local government. They are truly a group of ambitious entrepreneurs and operators that can compete globally. This bodes well for their foray into Europe starting this year (link).

You can spin the growth however you want, the reality is that DiDi, just like Uber China back in 2014, is buying up market share with promotions and subsidies. Here’s a chart of DiDi’s unit economics in international markets, taken from their IPO Prospectus (link)

You can see that DiDi’s take rate internationally is <10%, significantly lower than the normal 25% due to driver incentives. Moreover, they are also heavily promoting on the consumer side as well, regularly giving away trips at 50% off. How long can they keep that up when they are still losing billions of dollars in China every year?

On the point about competition, I agree that Uber has had a few hiccups in the region. This is partly due to the Covid pandemic wreaking havoc back in the US. Uber also wouldn’t give up Latin America (especially Mexico). It would effectively be the US allowing Soviets to set up missiles in Cuba. I believe Uber will come back around with a vengeance once they put out the fire. Can DiDi really afford to get into another capital war with Uber once they wake up?

Even if DiDi’s successfully, they likely wouldn’t be able to gain a monopoly in the market like in China, significantly limiting their pricing power and profitability in the local markets. Instead of the 26% take rate DiDi enjoys back home, I believe the take rate will settle around 15% in international markets (currently it’s at 10%).

What other adjacent verticals can DiDi get into in the future and how attractive can those businesses be?

DiDi is making long term bets on a number of areas that’s complimentary to their ride hailing business. They are taking a 3 prong approach .

- First they are expanding horizontally by adding additional transportation solutions for consumers (starting with bikes and e-bikes).

- Second, they are expanding vertically upstream, offering leasing, fueling and EV charging services to their drivers.

- Third, they are launching freight services to complement their existing business moving people.

Bike Sharing

Let’s talk first about their bike-sharing business. This is their largest initiative outside of their core business and one that’s the most mature. Bike-sharing is addressing a critical gap In DiDi’s ecosystem today, which is known as the first and last mile problem. Ridehailing is a great solution for distances > 3KM. But between 1 and 3 KM is often too close/expensive for cars, but too far to walk. Currently, most people either take the subway or the bus, but waiting for public transport sucks and space gets really cramped during rush hours. Biking would be a great alternative, but owning a bike is a hassle. They are underutilized assets (<5%) and are easily stolen. Bike sharing solves these concerns while giving riders greater convenience and freedom.

The concept was first introduced in 2014 by Ofo and caught on fire with the consumer. Almost overnight, millions of bikes lay out on the street and sidewalk to be rented by a simple scan of a QR code. However, in the pursuit of growth, excess is inevitable. By 2017, there was a massive oversupply of shared bikes clogging up sidewalks and streets, forcing the government to react and pass new regulations to control the situation. As governments tightened up, cyclists found themselves being hit with fines for riding on the sidewalk across cities of all sizes. In May, the 15th Beijing Municipal People’s At a neighborhood level, signs forbidding bike-share cycles went up on apartment complex gates, in commercial districts, and even in public parks. This effectively destroyed the bike sharing startup that relied on growth and VC funding to survive (link). By Dec 2018, Ofo officially declared bankruptcy and its competitor Mobike was acquired by Meituan for pennies on the dollar. and the subsequent bike share graveyard certainly wasn’t pretty at the time (link).

But despite this, bike sharing is not dead in the country. In fact, since regulations were introduced to manage supply and parking, the overall market resumed growth at a healthy rate (37% CAGR over the past 5 years) (link). As motor and battery technologies got more mature, electric bikes also took over a larger portion of the fleet each year.

DiDi is a relative late comer, only entering the market in 2018 through acquisition of Bluegogo. However, through their experience operating and scaling strong local network effect businesses, they were able to quickly grow to become the number 1 player in this market. According to an industry report by Analysys (link), they now have 35 million monthly active users, accounting for 42% market share.

More shared transport alternatives means DiDi can take larger shares of consumer’s travel and become a legitimate alternative to private car ownership. In China, bikes are a legitimate form of transport, not just for recreation use. Every day in China, there’s roughly 280 million “trips” taken. Of those trips, about 100 million are taken on bikes. Based on public usage data, I estimate that on average, each trip is on average 2KM, implying a total addressable market for bike sharing is $182B RMB ($28B USD). The addressable revenue in bike sharing ends up being similar in size to DiDi’s ride hailing business today once adjusted for driver pay. At current market share, this implies a 100% revenue upside and 200% upside in contribution margin in the next 3 to 5 years, with growth primarily coming from E-bikes. Over time, this model will extend to electric scooters as well, further expanding the market size.

Luckily, unlike the previous cycle, the unit economics of E-bike is significantly better. Because they are specifically intended for shared use, they are designed to be robust from the ground up. Moreover, since there’s a battery onboard, better power electronics can be attached for tracking and monitoring, dramatically increasing the efficiency of the fleet. The bikes are also tracked more rigorously, significantly reducing theft. Lastly, the players involved now are also much more rational with regards to subsidies compared to the last bike sharing cycle, so the market is no longer a race to the bottom.

Below is what the projected unit economics looks like for each bike.

With this kind of unit economics, the payback period is around 7 months and you see a cash on cash return of 400% return per year over the 3 year lifecycle! There aren’t many markets that can get this type of return at this scale.

Auto Solutions

DiDi’s suite of auto solutions is also one to watch. This business first started out of necessity as a driver acquisition and retention tool. Many people were willing to drive for DiDi, but didn’t have cars. To get drivers onto their platform, DiDi started a vehicle leasing platform (similar to Uber’s Xchange Leasing). As more drivers joined, they expanded to offer drivers more ways to save. DiDi started operating their own service hubs to give their drivers a cheaper and more reliable way to maintain their vehicles. They helped negotiate better insurance and fuel rates for their drivers across 6000 gas stations. When EV started picking up, they were one of the first to invest in a fast charging network at scale.

Currently, it has ~500,000 vehicles on its auto platform, covering all aspects of sale and after sale service. They have also built the largest public fast charging network in the country over the past 3 years. They now have over 20,000 DC fast chargers across the country, servicing over 500,000 registered EV (~20% of all EVs).

While both of these initiatives are still in their infancy and were incubated within the DiDi driver ecosystem, they are now opened up to the general public, which should give it additional upside and economies of scale. The same services that help DiDi drivers save money should also help regular consumers save. With some tweaks to the product, I think the suite of services will get the adoption it needs to really take off.

Intra-City Freight

DiDi’s last major initiative and the newest in the family is intra-city freight. The primary use case is moving. It’s a huge market, with estimated GMV worth $1 trillion RMB/year. Intra-city freight, like taxis prior to ride hailing, is highly fragmented and extremely opaque. Safety is also a big concern as people are letting strangers into their homes. It’s super early (DiDi only launched the service in August 2020), but early datas are promising. In certain pilot cities, it was able to achieve 50% market share within 2 months! (link)

While these new initiatives don’t come close in comparison to DiDi’s existing ride hailing business, they represent DiDi’s future and are each growing quickly. Each initiative has a large TAM, is operationally complex to manage, and can leverage DiDi’s existing business or expertise. They don’t all need to work, but if one of them hits, they can be as big or bigger than DiDi’s ride hailing business today in China.

DiDi is investing heavily into other segments to find additional growth, however, these businesses are all low margin commodity businesses with unattractive economics.

Bike sharing

For the bike sharing business, it certainly serves a very real need for consumers. However, the open question is: can this business actually make money? So far, it hasn’t and I believe the economics at steady state will be challenging.

With unit economics, the devil is in the details. I believe the assumptions above are overly optimistic, especially long term:

- On the revenue side, 6 average trips per day is too high. The addressable traditional bike trips market is ~100M trips/day. At 6 trips/day and implied 15 million total shared e-bikes in circulation (6 million DiDi e-bikes with 40% market share), it would mean shared e-bike have 90% penetration and will completely replace traditional bike ownership. A more reasonable assumption may be 4 trips/day.

- The prior model isn’t accounting for the loss rate at all. In the prior generation of bike-share companies, vehicle loss was a significant drag on return. These new e-bikes are significantly higher value and will attract much more attention from the bad actors.

- Prior maintenance cost is overly optimistic. Based on vehicle usage rate, each e-bike will see more than 13,000km of wear and tear. Just the brakes and tires alone likely cost that much. There’s also wear and tear on the motor as well as the battery, which is the most important part of the bike. These batteries alone are worth ~$2000 RMB. Unlike batteries in cars, batteries in e-bike are not liquid cooled. Furthermore, because they are parked outside in the elements, they are exposed to significant temperature variations, causing significant degradation. It’s likely that these batteries will need replacement every year.

With those revised assumptions, I re-calculated the unit economics of e-bike sharing. These numbers are much more pedestrian. Keep in mind, the contribution margin has to cover other fixed overhead like storage, insurance, sales & marketing, & corporate overhead. As you can see, the profit upside is significantly smaller.

Auto Solutions

As far as their leasing and energy business, I have limited hope that it’ll reach significant scale in the short and medium term. DiDi’s brand is associated with mobility, it will be tough to get consumer mind share for vehicle sales and service beyond its network of drivers. It’s also an area with lots of large and sophisticated competitors, from OEMs to large dealerships to independent service networks. While the market is large, it’s actually a highly efficient market with low single digit profitability. EV charging on the other hand, will end up being a huge market, but it’s still in its infancy and highly unprofitable in the short term. DiDi needs to strike a balance to ensure capital is deployed efficiently. Unlike services like bike sharing, basic infrastructure deployment is a marathon and the winner wouldn’t be apparent for another 5 to 10 years.

Intra-city Freight

Intra-city freight is perhaps the biggest opportunity for DiDi. The dynamics of the market is also similar to ride hailing so DiDi has a competitive advantage here. With that said, because it’s so similar to ride hailing, you can also expect massive competition and subsidies to come into play. To play to win, DiDi needs to prepare for the same “subsidy” war that occurred during the ride hailing and bike sharing saga. It’s also a brand new business and will take years and billions of dollars to reach scale. From a valuation standpoint, it would not be wise to give this initiative too much weight.

Overall, the 3 initiatives are either a:

a) terrible business with challenging unit economics

b) ok business but with limited upside and slow growth

c) business too new to ascribe substantial value to stock price currently.

Moreover, these initiatives are on track to burn $4B USD/year in 2021. Therefore, for rational investors that look for safety of margin, we should not ascribe significant values to these initiatives at the moment.

DiDi recently got hit with a regulatory probe and was forced to take its app down from China. What’s the regulatory risk for DiDi and how should I price that into the stock?

While this will certainly be a short-term headwind for DiDi, I believe for long term investors, the risk is overblown because your interest as an investor actually aligns well with China’s regulators. What China wants is healthy economic development and for its nation to get back to leadership on the global stage. As a result, over the past 2 decades, they have helped nurture a number of national champions set to take on the world. DiDi is one of them. Why would China purposely gut DiDi when it’s just starting to become an international powerhouse?

Of course, it’s important to have some regulations. DiDi is responsible for transporting people. They collect a lot of sensitive information they are collecting. Consumer protection and privacy laws have historically been lax in China, so it’s important to set clear guidelines that DiDi and other internet companies can follow. I believe that the regulatory probe this time is aimed at correcting that, and not a witch hunt to cripple the company like many have suggested.

In the short term, there will be some revenue loss. I believe that these headwinds are transitory and once DiDi meets the regulatory requirements, it’ll go back to business as usual. Moreover, given that existing users can still use the app fine and whoever needs to use DiDi likely already has the app downloaded, the impact to revenue should be limited.

If you are long China, you shouldn’t let this deter you away from investing in a company that has the potential to become a global powerhouse. Think of the recent volatility as a discount.

China is cracking down on big tech companies across the board. DiDi being a monopoly in the structurally important transportation sector, is a prime candidate for regulation. These national champion tech companies have become far too powerful, and are pursuing objectives that aren’t always in the best interest of the party, or specifically President Xi himself. Xi believes that the nation must act as one in order to advance its status on the global stage. No one person or company’s interest should be above the country’s. No one is allowed to publicly go against the party. It started with Jack Ma, and now he is trying to send a warning to everyone else: “I helped nurture you into what you are today. I can also destroy you in a heartbeat.” The risk isn’t DiDi going bankrupt, but that it will fall under the control of the Chinese government. As an investor, that means the company will be re-rated as a de-facto SOE (State Owned Enterprise), which trades at a significant discount (see China’s telecom or banking stocks relative to their US counterparts).

This isn’t the first time that Xi’s doing this. When he first came to power, he wielded a heavy stick and removed all his oppositions under the guise of “anti-corruption” (link). Was there corruption? Of course there is, but back in the days, you can pick anyone on the street and dig up corruption charges on them. Everyone bribed or took bribes at some point to get to where they are. That’s just how things worked. The anti-corruption campaign was a front for Xi to purge his opposition, reward his supporters, and gain the popularity of the public. Something similar is happening as Xi exerts his influence on the private sectors.

There’s no question that there will be increased scrutiny and regulation on China’s big tech going forward as Xi tries to gain control over them. Here are some developments that happened over the past 8 months:

- Regulator squash giant ANT IPO (link)

- China fine Alibaba record 275B for anti monopoly violation (link)

- China readies tencent antitrust penalty (link)

- China launches antitrust probe into Tencent backed property broker Beke (link)

- China opens antitrust probe on DiDi (link)

- China antitrust blocks Tencent backed merger between Huya and Douya (link)

- China launches antitrust probe into food delivery giant Meituan (link)

- China fines Tencent, Baidu and others over investment deals (link)

- China names 33 apps for unauthorized data collection (link)

The Chinese government may have let the kids run wild in the past, but there’s strong evidence that they are now keeping them on a tighter leash. Investors need to re-underwrite the regulatory risks associated with investing in Chinese stocks, particularly large and structurally important ones.

In terms of how to price the regulatory risks, it’s unfortunately more of an art than a science. I believe that a 25% discount to equivalent businesses in the US is a healthy margin of safety to account for the regulatory uncertainty. Unlike in other developed nations, one man can literally break your business.

DiDi is an incredibly impressive and important company for China. Management has an ambition to become a global leader in mobility. The company has a long term focus and strong operational capabilities. I believe the company is worth owning if the price is right.

However, with a current valuation of $52B USD, the company trades at the high end of fair value. I think there are stocks with better risk/reward ratios, but it’s low enough that it is worth monitoring the company’s progress.

Ultimately, below are some key factors that drove me to stay on the sideline for now:

- The China mobility business is stagnant with very little profitability to show for. Furthermore, I believe the ability to leverage its monopoly status and raise prices is limited. In addition, the recent app takedown by the regulators will stoke a new round of competition for ride hailing market share. I expect this will drastically reduce the unit’s profitability in the short term.

- The international business is growing nicely, but is unlikely to reach the dominant position that it has in China. Should DiDi gain majority market share, regulatory headwinds will get stronger as well, not only with taxi regulations, but also privacy regulations. Transportation data is inherently sensitive and poses national security risks.

- I believe the businesses within other initiatives can become successful. However, they are all high capex/opex, low margin businesses. With unit economics and industry dynamics similar to ride hailing, we can also expect extended periods of subsidy and losses. Can DiDi continue to fund these massive losses while its core business is still struggling to turn profit?

- While I don’t think the regulatory risk makes Chinese companies uninvestable, the fact that a single individual at the top can drastically change the rules is something that any investors should account for in their valuation framework. Given all else is equal, a company domiciled in the US should probably trade at a premium than one that’s domiciled in China.

Today, I think the business is worth ~$35B – $52B, which would imply a stock price of $7.4 – $11. It’s obviously a big range, but I believe it also reflects the variability in DiDi’s outcome. At current valuation, I believe it’s at the high end of fair value.

| Segment | Valuation (no brainer buy) | Valuation (buyer beware) |

| China mobility | $22B 3.5x P/S (Q1 2021 sales annualized) 10x P/ (Q1 2021 Adj. EBITDA annualized) | $33B 5x P/S (Q1 2021 sales annualized) 15x P/ (Q1 2021 Adj. EBITDA annualized) |

| International | $4B 8x P/S (Q1 2021 sales annualized) | $6B 12x P/S (Q1 2021 sales annualized) |

| Other initiatives | $9B 7x P/S (Q1 2021 sale annualized) | 13B 10x P/S (Q1 2021 sale annualized) |

| Total | $35B | $52B |

Key targets that would cause me to change my mind:

- Core ride hailing business resumes growth at 25%+ YoY without increasing take rate

- Demonstrated ability to take dominant market share against Uber in an international market

- 1 of the 3 other other initiatives starts contributing significantly to DiDi’s operating cashflow

Appendix

Addressable population China

| Total Population | 1,400,000,000 |

| Population 15 – 64 | 815,039,000 |

| % urbanization | 60% |

| addressable ride hailing market (people) | 489,023,400 |

Ride hailing addressable market – China

| Taxi travel distance per day (estimated) | 280 | source |

| Operating days / year | 360 | |

| Taxi travel distance per year (KM) | 100,800 | |

| number of taxis in China | 1,400,000 | source |

| total taxi miles | 141,120,000,000 | |

| average cost / mile (USD) | $0.50 | source, average fare from 20 1st tier and 2nd tier cities |

| China taxi GMV USD | $70,560,000,000 |

Ride hailing addressable market – Latin America

| Population | 650,000,000 | |

| Urban population | 80% | |

| Population between 15 and 65 | 65% | |

| Addressable population | 338,000,000 | |

| Average KM traveled in taxi / person / year | 138 | assume same frequency as China |

| Total KM traveled / year | 46,644,000,000 | |

| Average cost / km (USD) | $1.50 | source, average fare from the major cities within international markets |

| LatAm Taxi GMV (USD) | $69,966,000,000 |